The May 2021 edition of BDO’s Accounting Alert (click here) details the key aspects of the IFRIC decision.

The first question that the IFRIC decision looks at is whether the definition of an Intangible Asset is met which would facilitate costs associated with implementation services being able to be capitalised, noting that there are two criteria to be satisfied:

(i) That there is the power to obtain future economic benefits, and

(ii) That there is power to restrict others from having access to those same future economic

benefits.

It is here, particularly with respect to (ii), where entities have “gone wrong” in their previous determination that there is an Intangible Asset present to capitalise.

First assessment

The first thing to look at is whether the licensed software itself meets the definition of an Intangible asset.

If so, it is probably highly likely that any subsequent Implementation services would meet (i) and (ii) above.

Practicably this is likely to be the case if, and only if, the software in question is not off-the-shelf, or out-of-the-box software – that is, it is software that has been specifically built for a specific Customer.

However, even where this is the case, what would then need to be assessed is the rights around the intellectual property, IP, (i.e., the code) that has gone into building that software, and who has contractual rights (of use) to it.

If the Vendor retains IP rights to the software (and its code), then the Customer would typically be unable to demonstrate that (ii) has been met (i.e., the Vendor is not restricted from using the software code for the development of future software products for other potential customers).

If the IP is contractually protected for a period of time (i.e., the contract period), then it is arguable that the Customer satisfies (ii), but only for the period protected (which would then be the amortisation period of any Intangible asset recognised, unless the useful life of the software is shorter).

Assessing such IP protection would require specific analysis of the contract, as well as potential advice from legal experts regarding the legal and practical enforceability of such contractual clauses.

Second assessment

The second thing to look at is, even if the licensed software itself does not meet the definition of an Intangible asset (for the reasons above), whether the additional implementation services (most likely the customisation services) themselves meet the definition of an Intangible asset.

The analysis that needs to be done here is the same as in the First assessment above, being that an entity needs to consider and confirm whether the IP relating to the additional and/or modified code is contractual (and legally) protected, such that satisfaction of (ii) can be demonstrated.

Note that this Second assessment may still be necessary to consider even where the software itself does meet the definition of an Intangible asset (particularly if the contract is “silent” about specific aspects of the software build).

Treatment where costs are able to be capitalised as an Intangible Asset

Standard NZ IAS 38 accounting is applied, being that costs are capitalised and then amortised over the shorter of the licence period, IP protection period (if relevant), or the useful life of the software.

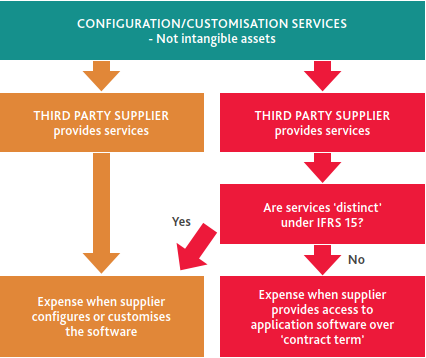

Treatment where costs are not able to be capitalised as an Intangible Asset

Again, this area was covered in some detail in the May 2021 edition of Accounting Alert (click here) with the below useful diagram:

The key point here is that even though there will be no Intangible Asset recognised, there may be instances where a Prepayment asset might be recognised (i.e., where amounts paid to the Vendor are in advance of the associated expense being recognised for accounting purposes).

The key difference between the three potential scenarios from the diagram above is the period over which the expense relating to the costs incurred for implementation services is spread, being:

- A shorter period (i.e., over the period that the services are provided) if the services are provided by:

- A third-party (i.e., different from the software Vendor), or

- The software Vendor, where the implementation services are “distinct” (see below)

- A longer period (i.e., over the licence “contract term”) if the services are provided by the software Vendor, where the implementation services are not “distinct”, i.e., “bundled” with the licence (see below).

It should be noted that the “contract term” itself is a matter that can be “grey” in practice, in particular where the licence is an open-ended (perpetual) licence.

Entities therefore need to consider which of the below guidance in NZ IFRS 15 is most appropriate in their particular situation:

- The period over which there are enforceable rights - were termination and renewal clause

analysis becomes critical), or

- The likely period over which the Customer will access the software, based on substance

(i.e., the use of the Customer’s unilateral rights to renew and/or terminate the licence).

Whether or not the implementation services are “distinct” requires an assessment of NZ IFRS 15 from the perspective of the software Vendor, with respect to identifying separate (“bundles” of) performance obligations.

These are explored further in section 3. below.