Public benefits entities: Assessing joint control

Financial reporting periods beginning on or after 1 January 2019 will bring a number of changes for Tier 1 and Tier 2 public benefit entities (“PBEs”), with a number of new PBE Standards coming into effect. Throughout 2019 we’ll examine these new standards through a series of articles in Accounting Alert.

The first new PBE Standard that we’ll examine is PBE IPSAS 37 Joint Arrangements (“PBE IPSAS 37”).

PBE IPSAS 37 Joint Arrangements

PBE IPSAS 37 supersedes PBE IPSAS 8 Interests in Joint Ventures (“PBE IPSAS 8.”). The adoption of PBE IPSAS 37 will result in the accounting for joint arrangements by PBEs becoming more closely aligned with the accounting treatment applied by for-profit entities reporting under New Zealand equivalents to International Financial Reporting Standards.

PBE IPSAS 37 comes into effect for annual financial reporting periods beginning on or after 1 January 2019, which means that, depending on your balance date, it is already in effect, or soon will be:

|

Balance date |

2018 year |

2019 year |

2020 year |

|

31 December |

Comparative period for adoption |

Year of adoption |

|

|

31 March |

|

Comparative period for adoption |

Year of adoption |

|

30 June |

|

Comparative period for adoption |

Year of adoption |

|

30 September |

|

Comparative period for adoption |

Year of adoption |

Early adoption of PBE IPSAS 37 is permitted as long as that fact is disclosed and all of the following new PBE Standards are also applied at the same time:

- PBE IPSAS 34 Separate Financial Statements

- PBE IPSAS 35 Consolidated Financial Statements

- PBE IPSAS 36 Investments in Associates and Joint Ventures

- PBE IPSAS 38 Disclosure of Interests in Other Entities.

PBE IPSAS 37 does three primary things:

- Defines what constitutes a joint arrangement

- Defines the two different types of joint arrangement

- Provides the accounting requirements for each of the two types of joint arrangement.

In this article we’ll examine what constitutes a joint arrangement. In future editions of Accounting Alert we’ll look at the other two key topics addressed in PBE IPSAS 37.

Joint arrangements

A joint arrangement is an arrangement that two or more parties have joint control of. A joint arrangement has two characteristics:

- The parties are bound by a binding arrangement

- The binding arrangement gives two or more of those parties joint control of the arrangement.

A binding arrangement is an arrangement that confers enforceable rights and obligations on the parties to it as if it were in the form of a contract. The binding arrangement sets out the terms upon which the parties participate in the activity that is the subject of the arrangement. The binding arrangement generally deals with such matters as:

- The purpose, activity and duration of the joint arrangement

- How the members of the joint arrangement’s governing body are appointed

- The decision-making process (the matters requiring decisions from the parties, the voting rights of the parties and the required level of support for those matters); this decision-making process establishes joint control of the arrangement

- The capital or other contributions required of the parties

- How the parties share assets, liabilities, revenues and expenses (or surplus or deficit) relating to the joint arrangement.

A binding arrangement is often, but not always, in writing (in the form of a contract or documented discussions between the parties). Statutory mechanisms, such as legislative or executive authority, can also create enforceable arrangements either on their own, or in conjunction with contracts between the parties.

Joint control

Joint control is the agreed sharing of control of an arrangement. There is joint control of an arrangement when all of the parties, or a group of the parties, to the arrangement, have all of the following in relation to the arrangement:

- Power over the arrangement, which exists when the parties have existing rights that give them the current ability to direct activities that significantly affect the nature or amount of the benefits from their involvement with the arrangement (those activities are referred to as the “relevant activities”)

- Exposure, or rights, to variable benefits from their involvement with the arrangement

- The ability to use their power over the arrangement to affect the nature or amount of the benefits from their involvement with the arrangement.

Joint control exists when decisions about the relevant activities require the unanimous consent of the parties sharing control, which means that joint control only exists where all the parties, or a group of the parties, to an arrangement must act together to direct the relevant activities.

Examples of activities that, depending on the circumstances, can be relevant activities include, but are not limited to:

- Using assets and incurring liabilities to provide services to service recipients

- Distributing funds to specified individuals or groups

- Collecting revenue through non-exchange transactions

- Selling and purchasing of goods or services

- Managing physical assets

- Managing financial assets during their life (including upon default)

- Selecting, acquiring or disposing of assets

- Managing a portfolio of liabilities

- Researching and developing new products or processes

- Determining a funding structure or obtaining funding.

Examples of decisions about relevant activities include, but are not limited to:

- Establishing operating and capital decisions of an entity, including budgets

- Appointing and remunerating an entity’s key management personnel or service providers and terminating their services or employment.

An arrangement can be a joint arrangement even though not all of its parties have joint control of the arrangement. In such circumstances, joint control only exists where the parties that have joint control are specified. This means, for example, that where there are five parties to an arrangement and four must agree to all decisions made regarding the relevant activities, joint control only exists where the parties that must agree are specified - joint control does not exist where the agreement of any four of the five parties to the arrangement is required for a decision to be made.

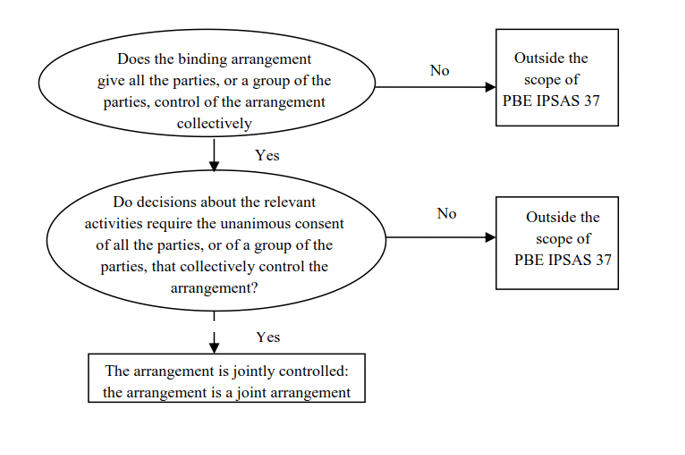

The diagram below (extracted from PBE IPSAS 37) demonstrates the steps for determining whether an arrangement is a joint arrangement and is consequently with the scope of PBE IPSAS 37:

The following examples illustrate joint control.

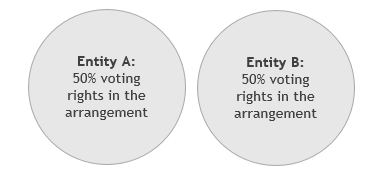

Example one:

Two entities (shown below) enter into a contractual arrangement; the terms of the arrangement stipulate that decisions about the relevant activities require the approval of Party A and Party B:

As both Party A and Party B must agree to decisions about the relevant activities, there is joint control and the arrangement is a joint arrangement.

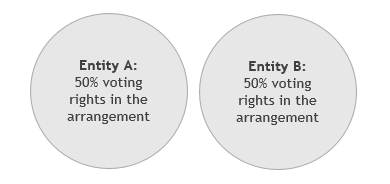

Example two:

Two entities (shown below) enter into a contractual arrangement; the terms of the arrangement stipulate that decisions about the relevant activities require 51% approval:

The only way to get 51% approval is for both Party A and Party B to agree. This means that there is joint control and the arrangement is a joint arrangement.

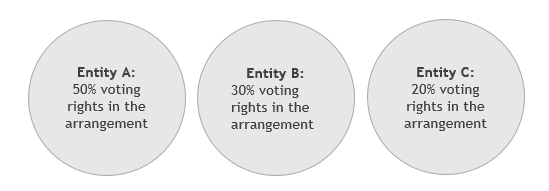

Example three:

Three entities (shown below) enter into a contractual arrangement; the terms of the arrangement stipulate that decisions about the relevant activities require at least 75% approval:

Decisions about the relevant activities require the approval of Entity A and Entity B (as between them they have 80% of the voting rights in the arrangement, which exceeds the 75% required for a decision to be approved). Decisions about the relevant activities can also be made if Entity A, Entity B and Entity C approve them, but the approval of Entity C is not required. The combined voting of Entity A and Entity C (70%) is not sufficient to reach the 75% threshold. This means that Entity A and Entity B have joint control of the arrangement and the arrangement is a joint arrangement.

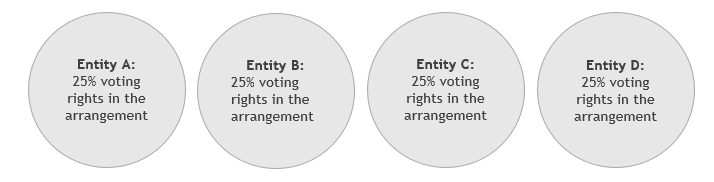

Example four:

Four entities (shown below) enter into a contractual arrangement; the terms of the arrangement stipulate that decisions about the relevant activities require at least 75% approval:

Decisions about the relevant activities require the approval of any three of the four parties to the arrangement. As joint control of an arrangement requires the parties that have joint control to be specified, joint control does not exist and the arrangement is not a joint arrangement (i.e. it is not within the scope of PBE IPSAS 37).

Example five:

Three entities (shown below) enter into a contractual arrangement; the terms of the arrangement stipulate that decisions about the relevant activities require a simple majority:

Decisions about the relevant activities can be made with the agreement of a number of different combinations of parties to the arrangement. As joint control of an arrangement requires the parties that have joint control to be specified, joint control does not exist and the arrangement is not a joint arrangement (i.e. it is not within the scope of PBE IPSAS 37).

Concluding thoughts

Determining whether joint control exists requires a thorough analysis of the terms and conditions of an arrangement. This often necessitates the analysis of documents such as constitutions and trust deeds and the application of considerable professional judgement. PBEs should commence the process of identifying potential joint arrangements as soon as possible, so that all relevant documents can be carefully reviewed. In addition, arrangements that are classified as jointly controlled assets, jointly controlled operations or jointly controlled entities under PBE IPSAS 8 should be analysed to ensure that they will classified as joint arrangements under PBE IPSAS 37.

For more on the above, please contact your local BDO representative.