Accounting for foreign exchange transactions in a non-hyperinflationary economy

Numerous entities transact with foreign entities or have subsidiaries and /or operations in foreign jurisdictions and are thus exposed to foreign exchange transactions. In addition, some entities are required to or elect to report in a presentation currency that is different to their functional currency. This article investigates how an entity is required to account for such foreign exchange transactions.

Which standard applies?

IAS 21 The Effects of Changes in Foreign Exchange Rates is the Accounting Standard that describes the requirements when accounting for foreign exchange transactions in a non-hyperinflationary economy. There are various interpretations that deal with specific aspects of foreign currency translation, but this article focuses on the basics of IAS 21. (Accounting for transactions in a hyperinflationary economy are accounted for under a different standard and are not addressed in this article.)

Scope of IAS 21

IAS 21 deals with how to:

- Account for transactions and balances undertaken by an entity in foreign currencies (except for derivatives accounted for under IFRS 9 Financial Instruments)

- Translate the results and financial position of foreign operations that have a different functional currency to the entity

- Translate the entity’s results and financial position into a presentation currency different to its functional currency.

Not in scope

IAS 21 does not apply to hedge accounting for foreign currency items (refer to IFRS 9 for this), and it also does not apply to hedging a net investment in a foreign operation (refer to IFRIC 16 Hedges of a Net Investment in a Foreign Operation for more guidance).

Key definitions

IAS 21 uses the following definitions, so it is important to understand what they mean before delving into the detailed accounting requirements.

|

Term

|

Definition

|

|

Closing rate

|

Spot exchange rate at the end of the reporting period

|

|

Exchange difference

|

Difference resulting from translating a given number of units of one currency into another currency at different exchange rates

|

|

Exchange rate

|

Ratio of exchange for two currencies

|

|

Foreign currency

|

Currency other than the functional currency of the entity

|

|

Foreign operation

|

An entity that is a subsidiary, associate, joint arrangement or branch of a reporting entity, the activities of which are based or conducted in a country or currency other than those of the reporting entity

|

|

Functional currency

|

Currency of the primary economic environment in which the entity operates

|

|

Monetary items

|

Units of currency held and assets and liabilities to be received or paid in a fixed or determinable number of units of currency

|

|

Net investment in a foreign operation

|

Amount of the reporting entity’s interest in the net assets of that operation

|

|

Presentation currency

|

Currency in which the financial statements are presented

|

|

Spot exchange rate

|

Exchange rate for immediate delivery

|

Functional currency versus presentation currency

When preparing general purpose financial statements, it is important to understand the difference between your entity’s ‘functional currency’ and its ‘presentation currency’.

An entity measures transactions and balances in its financial statements using the functional currency, which is the currency of the primary economic environment in which the entity operates. The presentation currency is the currency used when presenting the financial statements.

For example, a New Zealand entity that mainly does business in New Zealand, and mainly transacts in New Zealand dollars, will have a New Zealand dollar functional currency, and will usually also have a New Zealand dollar presentation currency. However, it may choose a different presentation currency if desired (IAS 21.18 and 19).

Determining functional currency is not always straight forward

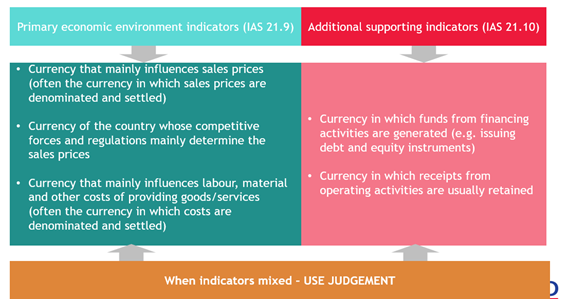

It is not always easy to determine an entity’s functional currency because it may transact in several currencies. However, IAS 21, paragraphs 9-11, include a hierarchy of indicators to help entities decide on the appropriate functional currency. These indicators are:

- Step 1 – Consider the primary economic environment indicators (IAS 21.9)

- Step 2 – Consider additional supporting indicators (IAS 21.10)

- Step 3 – When indicators are mixed, use judgement.

The hierarchy gives more importance to paragraph 9 than paragraph 10. Therefore, if an entity’s revenues and costs associated with generating those revenues are impacted by US dollar movements, this is more significant for determining the entity’s functional currency than the entity’s funding arrangements.

Example 1

A New Zealand parent company has the majority of its revenue earning activity being by way of dividends received from its overseas subsidiaries. It is very unlikely to have a New Zealand dollar (NZD) functional currency, even though it raises funding from New Zealand investors.

Example 2

Mining Co is listed in New Zealand and has a gold mine in South Africa.

The South African workforce is paid in South African Rands and capital equipment is purchased in US dollars.

The gold produced by the mine is sold in US dollars. Mining Co is financed by loans in New Zealand dollars, it incurs listing fees in New Zealand and pays its directors in New Zealand.

Analysis

The functional currency of Mining Co is US dollars because:

- This is the currency that mainly influences sales prices for goods and services, and the gold price is denominated and settled in US dollars

- While labour costs are incurred in South African Rands, the currency that mainly influences the material and other costs of providing goods or services is arguably US dollars because capital equipment is purchased in US dollars.

The additional factors contained in paragraph 10 regarding funding and corporate costs in New Zealand dollars are not considered because management gives priority to the primary indicators in paragraph 9.

Do all entities in a group have the same functional currency?

No. Each entity prepares its standalone financial statements by measuring its transactions and balances in its own functional currency. However, when preparing consolidated financial statements, or when an individual entity has a branch that is a ‘foreign operation’, the parent entity translates the foreign currency items into its own functional currency (refer below for more information).

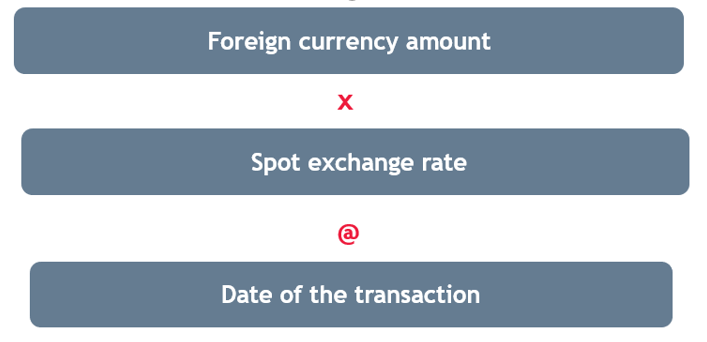

Initial recognition of foreign currency transactions

Foreign currency transactions are initially recorded in the entity’s functional currency by applying the spot exchange rate to the foreign currency amount on the date of the transaction.

The date of the transaction is the date the transaction qualifies for recognition in accordance with other Accounting Standards. Practically, a rate that approximates the actual rate on the date of the transaction is often used, for example, an average rate for the month, but using average rates is not appropriate where there are significant fluctuations in the exchange rate during the period.

Subsequent recognition - monetary items

At the end of each subsequent reporting period, any foreign currency monetary items are translated using the closing rate, or spot rate at the end of the reporting period.

What are monetary items?

‘The essential feature of a monetary item is a right to receive (or an obligation to deliver) a fixed or determinable number of units of currency. Examples include: pensions and other employee benefits to be paid in cash; provisions that are to be settled in cash; lease liabilities; and cash dividends that are recognised as a liability. Similarly, a contract to receive (or deliver) a variable number of the entity’s own equity instruments or a variable amount of assets in which the fair value to be received (or delivered) equals a fixed or determinable number of units of currency is a monetary item. Conversely, the essential feature of a non-monetary item is the absence of a right to receive (or an obligation to deliver) a fixed or determinable number of units of currency. Examples include: amounts prepaid for goods and services; goodwill; intangible assets; inventories; property, plant and equipment; right-of-use assets; and provisions that are to be settled by the delivery of a non-monetary asset.’

IAS 21, paragraph 16

Subsequent recognition - non-monetary items

Non-monetary items are recognised at the end of each subsequent reporting period as follows:

· If measured at historical cost in a foreign currency - translated using the exchange rate at the date of the transaction

· If measured at fair value in a foreign currency - translated using the exchange rate when the fair value was determined.

Where is the exchange difference recognised?

Monetary items

Exchange differences on monetary items may arise from:

1. Translating unsettled monetary items at the end of a reporting period at closing rates different to the spot rates used at initial recognition (unrealised exchange differences)

2. Settling monetary items at an exchange rate different to that used for initial recognition (if settled in the same accounting period the item is first recognised), or that is different to that used for subsequent recognition as noted above (realised exchange differences).

These exchange differences are recognised in profit or loss in the period they arise, however, if they form part of a hedging relationship, they are accounted for under IFRS 9.

Non-monetary items

When the fair value of a non-monetary item is measured using a foreign currency (for example, a property held overseas where fair value is determined in the currency of the foreign jurisdiction), as noted above, the exchange rate used to determine fair value in the functional currency is the rate at the date when fair value was determined. This could differ from the original rates used to translate the item and results in an exchange difference.

IAS 21 requires the exchange difference component of the fair value movement on a non-monetary item to be recognised in the same way as the fair value movement. For example, the exchange component of a revaluation increment for PPE is recognised in other comprehensive income (OCI) but is recognised in profit or loss for investment property.

Net investment in a foreign operation

As noted above, exchange differences arise when an entity borrows or lends money in a currency different to its functional currency and these are recognised in profit or loss because the exchange difference relates to a monetary item.

If such transactions occur between group entities, and settlement is neither planned nor likely to occur in the foreseeable future, in substance, this forms part of the entity’s ‘net investment in that foreign operation’. In such cases, exchange differences on the foreign currency receivable or payable are recognised as follows:

- In separate or individual financial statements – in profit or loss

- In financial statements that include the foreign operation (e.g., the consolidated financial statements if foreign operation is a subsidiary) – in OCI (foreign currency translation reserve).

That is, on consolidation, the exchange difference recognised is removed from profit or loss and recognised in OCI. Any amounts recognised in OCI on consolidation are only reclassified and recognised in profit or loss on disposal of the net investment.

Amounts considered part of the net investment in a foreign operation may include long-term receivables or loans, but not trade receivables or trade payables. It is important to note that to be considered part of the entity’s net investment in a foreign operation, settlement must be neither:

- Planned, nor

- Likely to occur in the foreseeable future.

What if an entity changes its functional currency?

An entity only changes its functional currency if there has been a change in facts and circumstances regarding the underlying transactions, events and conditions (refer to the discussion above regarding the hierarchy of factors to consider).

The effect of changing functional currency is accounted for prospectively from the date of change.

Presentation currency is different to the functional currency

Where an entity chooses a presentation that is different to the entity’s functional currency, it must go through a process to translate the functional currency financial statements into the presentation currency. Where the functional currency is not considered hyperinflationary, the process is as follows:

- Assets and liabilities – Translate at the closing rate for each balance sheet presented

- Income and expenses – Translate at exchange rates at the dates of the transactions (can use average rates unless there has been a significant fluctuation in exchange rates during the period)

- Resulting exchange differences – Recognised in OCI (foreign currency translation reserve).

Translating results and financial position of foreign operations

If a foreign operation (e.g., subsidiary or a branch) has a different functional currency to the entity (parent entity), its results and financial position must be translated into the presentation currency of the reporting entity (parent entity in the case of a group). The process is the same as that described above for translating the functional currency into a different presentation currency. In addition:

- Any exchange differences recognised in profit or loss that are part of the entity’s net investment in foreign operation are removed from profit or loss and recognised in OCI (refer discussion above for more information)

- Goodwill and any fair value adjustments to assets and liabilities arising on the acquisition of a foreign operation are treated as assets and liabilities of the foreign operation. This means they are expressed in the functional currency of the foreign operation and translated at the closing rate.

Disposals or partial disposals of foreign operations

On the disposal of a foreign operation, the cumulative exchange difference recognised in OCI is reclassified to profit or loss.

Disposal may be through sale, liquidation, repayment of share capital, or abandonment of all or part of that entity. A write-down to the carrying amount of a foreign operation does not constitute a partial disposal, so no part of the exchange difference recognised in OCI may be reclassified to profit or loss at the time of the write-down.

The rules for reclassifying the exchange differences recognised in profit or loss to OCI are complicated where there is a partial disposal. Please contact BDO’s IFRS Advisory Team us if you need assistance in this regard.

What about foreign currency cash flows in the cash flow statement?

IAS 21 does not apply to presentation of foreign currency cash flows in the cash flow statement. Instead, IAS 7 Statement of Cash Flows requires:

- Cash flows arising from transactions in a foreign currency are to be recorded in an entity’s functional currency by applying the exchange rate at the date of the cash flow (in practice this can be an average rate)

- Cash flows of a foreign subsidiary are to be translated at the exchange rates between the functional currency and the foreign currency at the dates of the cash flows.

In practice, entities are permitted to use a rate that approximates the actual rate, such as the weighted average exchange rate for the period.

Unrealised gains and losses arising from changes in foreign currency exchange rates (e.g., translating a foreign currency borrowing to spot rate at reporting date) are not cash flows and are therefore not usually reported in the cash flow statement. However, if the entity holds a balance of cash and cash equivalents in a foreign currency (such as a New Zealand entity holding a USD bank account), movements in the exchange rate are reported at the bottom of the cash flow statement.

Example

NZ Co has a New Zealand dollar (NZD) functional currency and has a USD bank account with a balance of USD 70 at financial years ending 31 December 2020 and 2021. The NZD:USD exchange rates are as follows:

- 31 December 2020 USD:NZD 0.7:1.0 = NZD 100

- 31 December 2021 USD:NZD 0.8:1.0 = NZD 87.50.

When NZ Co presents its cash flow statement in NZD at 31 December 2021, it has effectively ‘lost’ $12.50 because the USD 70 bank account is now only worth $85.50 compared to $100 one year ago.

At the bottom of NZs Co’s cash flow statement for the year ended 31 December 2021, it would show:

|

|

$NZD

|

|

Cash and cash equivalents at the beginning of the year

|

100

|

|

Effects of exchange rate changes on cash and cash equivalents

|

(15)

|

|

Cash and cash equivalents at the end of the year

|

85

|

Need assistance with complex foreign exchange transactions?

In practice dealing with foreign exchange transactions can be complex, particularly when changing your functional currency or presentation currency, or even just preparing your consolidated financial statements that include foreign operations.

Please contact BDO’s IFRS Advisory Team if you require assistance.